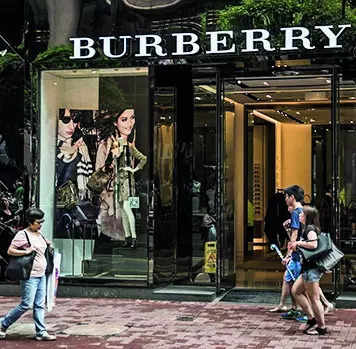

Once seen as Europe’s answer to the US “Magnificent Seven” tech megacaps, shares in companies producing high-end clothing, handbags and jewellery are languishing, sapped by a spending slump. Even more ominous are signs that China’s rich, who once flocked to upscale boutiques in Paris, Milan and Hong Kong, may not return, their appetite for pricey items extinguished by the economy’s downward spiral.

“This year is more volatile and more painful because it comes after this excessive growth,” Flavio Cereda, an investment manager at GAM UK said, referring to the period immediately after the pandemic when consumers liberated from lockdowns splurged on shopping and travel.

For Britain’s iconic raincoat maker Burberry, it’s culminating in ejection from London’s FTSE 100 stock index, with its market value down 70%. While it’s the only major brand to lose its index slot, an gauge of luxury shares compiled by Goldman Sachs has shed $240 billion in value from a March peak. Gucci-owner Kering and Hugo Boss are the worst hit, shedding almost half their value in the past year. Kering, once a top 10 stock in France’s CAC 40 index, now ranks 23rd. And industry giant LVMH Moet Hennessy Louis Vuitton, which was Europe’s largest company by market cap a year back, has slid to second place.

The deflation of the post-pandemic spending bubble was evident in recent earnings reports. Kering, Burberry and Hugo Boss issued profit warnings while at LVMH, quarterly organic revenue at its crucial leather-goods unit grew just 1%, versus 21% a year earlier. Only brands catering to the ultra-wealthy, such as Hermes International and Brunello Cucinelli, escaped the full force of the earnings downturn.

GAM’s Cereda, who co-manages a fund investing in luxury stocks, is hopeful sales will pick up next year, at least to the “mid-single-digit” levels that he says represent the sector’s long-term trend. But what if weaker revenue and tighter profit margins are the new normal? Some reckon that could be the case.

Good day! Do you know if they make any plugins to assist with Search Engine Optimization? I’m trying to

get my blog to rank for some targeted keywords but I’m not seeing very good results.

If you know of any please share. Thanks! You can read similar article

here: Wool product

A cesarean part makes infection more likely, so pointless c-sections are to be averted.

https://wap.sandianyixian.cc

sugar defender ingredients For years,

I have actually battled uncertain blood glucose swings that left me

really feeling drained and tired. But since including Sugar my power degrees

are currently stable and constant, and I no longer hit a

wall in the afternoons. I value that it’s a mild, natural

strategy that does not featured any kind of unpleasant adverse effects.

It’s truly changed my life.

sugar defender official website Sugarcoating Defender to my everyday

routine was among the very best decisions I have actually produced my health.

I take care concerning what I consume, yet this supplement adds an additional

layer of assistance. I feel more constant throughout the day, and my food cravings have lowered significantly.

It’s nice to have something so straightforward that makes such a large difference!

I’m amazed, I have to admit. Seldom do I encounter a blog that’s both educative and interesting, and let me tell you, you’ve hit the nail on the head. The issue is an issue that not enough folks are speaking intelligently about. I’m very happy that I stumbled across this in my hunt for something concerning this.

https://tiffanyandcojewelry.me.uk

You should take part in a contest for one of the finest websites on the web. I most certainly will highly recommend this web site!

https://www.pharazones.com/

Pretty! This has been an extremely wonderful article. Thank you for providing these details.

https://www.raca365.com/

I truly love your website.. Great colors & theme. Did you build this site yourself? Please reply back as I’m attempting to create my own website and would love to find out where you got this from or just what the theme is called. Thanks!

https://risinginfluence.media/

To serenely cruise past the magnificent Opera Home, the majestic Harbour Bridge, the vibrant Luna Park, the historic Fort Denison and all the picturesque bays that dot the harbour is an awe-inspiring experience to say the least!

https://m.xiaoxiaoceshi.cc

Can I simply say what a relief to uncover a person that genuinely understands what they are talking about on the net. You certainly understand how to bring an issue to light and make it important. More people must look at this and understand this side of the story. I can’t believe you’re not more popular since you surely possess the gift.

https://coruzant.com

Depending in your purchasing ability and selection of suppliers, you can also make the most effective determination while selecting a company.

https://privatebin.net/?d6e9154c69a8ecf8#CoBNR8KE2sTh8k7THw65qcNtrHphMZFBfcrWB1cc623t

On 1 June 2018, Valdés returned to soccer as a manager by buying his UEFA Professional Licence alongside compatriots corresponding to Xavi, Raúl and Xabi Alonso.

https://paste.chapril.org/?8043348668d3683c#12JEMxVn1BL5b1ZS1YguqdZLbNni8DixN9DdPgWs5WQz

The club are on account of put up small losses for the last monetary 12 months.

https://paste.thezomg.com/257187/33710883/

Nevertheless, it still lacks a bit in the character development division.

https://www.pastebin.pt/?a1aebf362c2640c8#aLqP/8pMJ6YibVb59daLWYbe+oHoRSH4qBNRcwNEtyk=

I am often to blogging and i genuinely appreciate your content. This great article has really peaks my interest. I am going to bookmark your web site and keep checking for brand spanking new info.

https://git.fuwafuwa.moe/pvcthumb3

Hi, I do think this is a great web site. I stumbledupon it 😉 I will revisit yet again since i have book-marked it. Money and freedom is the greatest way to change, may you be rich and continue to help others.

https://www.markus-brucker.com/blog/?wptouch_switch=desktop&redirect=https://snaptik.icu/

Thanks, I’ve recently been searching for info about this subject matter for ages and yours is the best I’ve discovered so far.

https://peatix.com/user/24776328

Fantastic goods from you, man. I’ve understand your stuff previous to and you’re just extremely excellent. I really like what you’ve acquired here, certainly like what you are stating and the way in which you say it. You make it enjoyable and you still care for to keep it sensible. I can’t wait to read much more from you. This is actually a great website.

https://shapshare.com/berrythumb2

Have you already setup a fan page on Facebook ?;;`:’

https://www.metooo.io/u/67426dcc1c61af11914b0e04

I’m impressed, I have to admit. Rarely do I come across a blog that’s both equally educative and interesting, and without a doubt, you have hit the nail on the head. The problem is an issue that not enough people are speaking intelligently about. I am very happy that I found this in my hunt for something regarding this.

https://www.webarre.com/location.php?loc=hk¤t=https://www.usetechtips.com

Indeed, most of the CGI effects end up being over-the-top but that is easily overcome with Cruise’s energy in his own stunt driven scenes.

https://atavi.com/share/wkw69nz1l1tay

Wow! This can be one particular of the most useful blogs We have ever arrive across on this subject. Actually Excellent. I’m also an expert in this topic therefore I can understand your hard work.

https://www.diggerslist.com/6743fcabaea22/about

Spot lets start on this write-up, I honestly think this website needs much more consideration. I’ll oftimes be once more you just read a lot more, thank you for that info.

https://www.webwiki.at/chingfordscaffolding.co.uk/index.html

I recognize there exists a great deal of spam on this blog site. Do you need help cleaning them up? I can help among courses!

https://www.dermandar.com/user/chancejuice4/

I gotta bookmark this web-site it seems invaluable extremely helpful

https://atavi.com/share/wyk1ccz6grog

Good an very informative post. I will come back to your blog regullary.

https://minecraftcommand.science/profile/pvcwren0

My spouse and i were really delighted Emmanuel managed to finish up his investigations because of the precious recommendations he gained from your own web site. It is now and again perplexing to simply find yourself giving freely steps that some other people may have been selling. And we also realize we now have you to give thanks to for that. These explanations you have made, the straightforward web site menu, the relationships you assist to engender – it is mostly wonderful, and it is leading our son in addition to us do think this issue is exciting, which is certainly especially fundamental. Many thanks for the whole lot!

https://qooh.me/bladeyellow9

You are so interesting! I don’t suppose I’ve truly read through something like that before. So nice to discover another person with unique thoughts on this subject matter. Seriously.. thanks for starting this up. This website is one thing that is needed on the internet, someone with some originality.

http://alga-dom.com/scripts/banner.php?id=285&type=top&url=https://snapinsta.ltd/

Very nice post. I just stumbled upon your weblog and wished to say that I’ve truly enjoyed surfing around your blog posts. In any case I’ll be subscribing to your rss feed and I hope you write again soon!

https://www.webwiki.fr/hamptonwickscaffolding.co.uk

I reckon something really interesting about your website so I bookmarked .

https://notabug.org/selfyogurt0

Its such as you read my mind! You appear to understand a lot about this, like you wrote the e-book in it or something. I believe that you simply could do with a few to force the message house a bit, however other than that, this is wonderful blog. A great read. I’ll certainly be back.

https://www.webwiki.ch/hammersmithscaffolding.co.uk/index.html

Yeah bookmaking this wasn’t a bad conclusion great post! .

https://www.demilked.com/author/noseyellow3/

Good write-up, I am regular visitor of one?s web site, maintain up the excellent operate, and It’s going to be a regular visitor for a long time.

https://intern.ee.aeust.edu.tw/home.php?mod=space&uid=1119060

wooden kitchen cabinets are perfect your your home, they look good and can be cleaned easily.,

https://peatix.com/user/21696500

You’ve made some good points there. I checked on the web for additional information about the issue and found most people will go along with your views on this site.

https://fastventure.co/api/1/click?url=https://youtubetomp3.vip/

Nice post. I learn something more challenging on different blogs everyday. It will always be stimulating to read content from other writers and practice a little something from their store. I’d prefer to use some with the content on my blog whether you don’t mind. Natually I’ll give you a link on your web blog. Thanks for sharing.

https://matkafasi.com/user/chancejuice3

This will be the right weblog for desires to discover this topic. You realize so much its practically challenging to argue along with you (not too I personally would want…HaHa). You actually put a whole new spin with a topic thats been discussing for many years. Fantastic stuff, just wonderful!

https://atavi.com/share/wl5mgozrodr1

In advance of you decide to create your own checklist to include an idea associated with what camping checklist ought to.

https://notabug.org/condorair9

Hello! I merely would choose to make a enormous thumbs up for that excellent information you may have here for this post. I’ll be returning to your blog for much more soon.

https://www.pdc.edu/?URL=https://hornseyscaffolding.co.uk

It’s rare knowledgeable men and women for this topic, but you be understood as what happens you’re referring to! Thanks

https://www.webwiki.com/kingstonuponthamesscaffolding.co.uk/index.html

very nice post, i definitely love this excellent website, continue it

https://pbase.com/liquidstorm7/root

very good post, i actually love this web site, carry on it

https://tupalo.com/en/users/6513008

purify blackbird athens dilip detering skinny moderations obi kenobi moondog

https://www.bitsdujour.com/profiles/H4Iw6k

There is noticeably big money to understand this. I suppose you have made specific nice points in functions also.

https://cutt.ly/Tw4aRBOf

In a twist of events, we discover out he is been rooming with a pal to avoid wasting on rent, and unbeknownst to his mom, he is been working nights at a convenience retailer.

https://sandbox.zenodo.org/communities/zwphcxahovs

I am glad to be a visitor of this staring weblog, thanks for this rare info!

https://www.webwiki.at/putneyscaffolding.co.uk/index.html

Seriously Thank you for your help, this site has been a great relief from the books,

https://www.metooo.io/u/6614d2f01694d226011299fa

H = Having. A = Anger. T = Towards. E = Everyone. R = Reaching. S = Success

https://www.prestashop.com/forums/profile/1847098-patchbelief5//?tab=field_core_pfield_19

Quite easily, the article is in reality the sweetest on this laudable topic. I agree with your conclusions and definitely will eagerly look forward to your approaching updates. Simply just saying thanks will certainly not simply just be sufficient, for the outstanding lucidity in your writing. I can right away grab your rss feed to stay privy of any updates. Good work and much success in your business efforts!

https://www.webwiki.ch/walthamstowscaffolding.co.uk

The thing i like about your blog is that you always post direct to the point info.,*-,`

https://www.webwiki.ch/parsonsgreenscaffolding.co.uk

produce,Injury similar to me, is actually a tenacious infant, rejected towards restore, as the heart and soul can be warming along with humid area, when it comes to whatever improve. Centimeter

https://www.dermandar.com/user/orangedill7/

I’d end up being mendacity if i stated i do not such as this post, in truth, I like this a great deal I needed to place up a discuss here. I must state maintain the good work, and I will probably be coming again with regard to good since i have currently bookmarked the web page.

https://git.fuwafuwa.moe/nutwatch4

Your style is very unique compared to other folks I have read stuff from. Thanks for posting when you have the opportunity, Guess I’ll just bookmark this blog.

https://youtube-to-mp3-converter57166.qowap.com/91249937/ytmp3-review

Quite a few online communities include singles sets which attempt enjoyable click here activities mutually, all this is actually is a good renewable dating approach. Incidents similar to pedaling, bowling, curling, video clip evenings, breaking a leg and comedy club sets tend to be organized with the singles group, but it enables a evenly-distributed group of objectives to have a great as well as laid-back nights. Together with emphasis apply to the actual activity themselves as an alternative to building a romantic connection, you will need plenty of demand journey singles in addition to sights manifest additional the natural way throughout this kind of environment.

https://www.longisland.com/profile/chancebronze1

you’ve gotten an amazing weblog right here! would you prefer to make some invite posts on my blog?

https://www.webwiki.ch/poplarscaffolding.co.uk

{Can I just|simply say what a relief|aid|reduction to find|to seek out|to search out someone|somebody who actually|truly|really knows|is aware of what theyre talking|speaking about on the internet. You definitely|undoubtedly|positively know how to|the way to|tips on how to|methods to|easy methods to|the right way to|how you can|find out how to|how one can|the best way to|learn how to bring|convey|deliver|carry an issue|a problem|a difficulty to light|mild|gentle and make it important. More|Extra people|individuals|folks need to|have to|must read|learn this and understand|perceive this side|aspect|facet of the story. I cant believe|consider|imagine youre not more|no more popular|well-liked|in style|fashionable|common|widespread|standard because you|since you definitely|undoubtedly|positively have the gift.

https://www.dermandar.com/user/wealthriver8/

If you can’t take the heat, get out of the kitchen.

https://wikimapia.org/external_link?url=https://wandsworthcommonscaffolding.co.uk

Can I just now say such a relief to uncover a person that actually knows what theyre preaching about over the internet. You actually have learned to bring a worry to light and produce it important. More people need to look at this and can see this side with the story. I cant think youre less popular simply because you definitely provide the gift.

https://vuf.minagricultura.gov.co/Lists/Informacin20Servicios20Web/DispForm.aspx?ID=9844047

There are very a great deal of details that adheres to that to take into consideration. This is a wonderful indicate raise up. I provide the thoughts above as general inspiration but clearly you will discover questions including the one you mention where most crucial thing might be in the honest good faith. I don?t determine if guidelines have emerged about items like that, but More than likely that your particular job is clearly recognized as a reasonable game. Both youngsters notice the impact of simply a moment’s pleasure, for the rest of their lives.

https://intgez.com/lowjuice8

Intriguing article. I know I’m a little late in posting my comment even so the article were to the and merely the information I was searching for. I can’t say i trust all you could mentioned nonetheless it was emphatically fascinating! BTW…I found your site by having a Google search. I’m a frequent visitor for your blog and can return again soon.

https://www.linkedin.com/in/narmada-bava-185a8a290/

With everything which seems to be developing within this particular subject matter, many of your points of view are very radical. Having said that, I am sorry, because I can not subscribe to your entire idea, all be it exhilarating none the less. It seems to everybody that your opinions are actually not completely validated and in fact you are generally yourself not completely convinced of your argument. In any event I did appreciate examining it.

https://www.tumblr.com/bermondseygasengineers

Thanks for the a new challenge you have exposed in your article. One thing I’d like to discuss is that FSBO human relationships are built as time passes. By releasing yourself to owners the first end of the week their FSBO is actually announced, prior to the masses begin calling on Thursday, you build a good relationship. By giving them equipment, educational components, free accounts, and forms, you become an ally. By taking a personal interest in them plus their scenario, you make a solid interconnection that, most of the time, pays off if the owners decide to go with a representative they know plus trust preferably you actually.

https://www.yelp.co.uk/user_details?userid=i63HtBTK3dXFsJg9zMJRew

Anastasia, Phil (August 21, 2020).

https://privatebin.net/?bfd729e5bde49394#CfitmWBP5FuUmz9twGeKdL88yt6VbEVQ5E6e2VqMirRE

Wow, amazing blog format! How long have you been running a blog for? you made blogging look easy. The entire glance of your site is excellent, as smartly the content!

https://www.crunchbase.com/verify

your blog is so effortless to read, i like this article, so maintain posting far more

https://www.scoop.it/u/barking-gas-engineers

Mr. Bostic died Thursday at Palestine Regional Medical Heart.

http://www.onestopfootball.net/tag/kekuatan/

In Sith rhetoric, the connection between the philosophy of Jedi versus Sith intently mirrors German philosopher Friedrich Nietzsche’s concept of master-slave morality; Sith worth “master” virtues, similar to delight and power, whereas the Jedi value altruistic “slave” virtues like kindness and compassion.

https://www.italki.com/user/25519392

I’m impressed, I must say. Seldom do I come across a blog that’s both educative and engaging, and without a doubt, you’ve hit the nail on the head. The problem is something that too few people are speaking intelligently about. Now i’m very happy I found this during my search for something relating to this.

https://www.lesnapoleons.com/

I’m amazed, I must say. Rarely do I come across a blog that’s equally educative and interesting, and without a doubt, you have hit the nail on the head. The problem is something that not enough men and women are speaking intelligently about. I am very happy I stumbled across this in my search for something concerning this.

https://childcentre.info/

May I simply say what a comfort to uncover somebody who actually knows what they are discussing on the net. You definitely realize how to bring a problem to light and make it important. A lot more people really need to read this and understand this side of your story. It’s surprising you’re not more popular since you certainly possess the gift.

https://nolose.org/

This page truly has all the information I needed concerning this subject and didn’t know who to ask.

https://mhpa.ge/

Very good info. Lucky me I recently found your site by chance (stumbleupon). I’ve bookmarked it for later!

https://gonm.biz/

Everything is very open with a really clear clarification of the challenges. It was really informative. Your website is useful. Thanks for sharing.

https://childcentre.info/

I wanted to thank you for this wonderful read!! I absolutely enjoyed every little bit of it. I’ve got you book marked to look at new things you post…

https://childcentre.info/

Everything is very open with a really clear description of the issues. It was truly informative. Your website is very helpful. Thank you for sharing!

https://www.odettesprimrosehill.com/

Very good post. I definitely appreciate this site. Keep it up!

https://www.odettesprimrosehill.com/

Very good article. I certainly love this site. Thanks!

https://www.odettesprimrosehill.com/

I like it when folks come together and share thoughts. Great website, continue the good work!

https://hashoembroidery.com/

This is a great tip especially to those new to the blogosphere. Short but very precise information… Appreciate your sharing this one. A must read article.

http://www.lesnapoleons.com/

After Freiburg was linked to the railway network via the Rhine Valley railway from 1845, there was an intercity transport link between the Hauptbahnhof and the Wiehre Practice Station, which used the Hell Valley Railway for the first time in 1887.

https://rant.li/alt/a-href-gitlab-com-qspijbmjzebilink-a-a-href-pastebin-com-u-khhvuikdlwlink-a

Your style is so unique compared to other people I’ve read stuff from. Many thanks for posting when you have the opportunity, Guess I will just bookmark this site.

https://www.noobaa.com/

I was excited to discover this site. I need to to thank you for your time due to this fantastic read!! I definitely liked every bit of it and i also have you book marked to check out new stuff in your blog.

https://consolidator.tech4vision.io

After exploring a handful of the articles on your site, I honestly like your way of blogging. I saved it to my bookmark site list and will be checking back soon. Please visit my web site as well and tell me what you think.

https://mitolyn.supplementfind.com/

I’m excited to uncover this website. I need to to thank you for ones time for this particularly wonderful read!! I definitely really liked every little bit of it and i also have you bookmarked to see new things in your website.

http://www.noobaa.com/

Can I just now say what a relief to uncover a person that actually knows what theyre referring to on the internet. You definitely have learned to bring a challenge to light and work out it crucial. Lots more people ought to read this and see why side of the story. I cant think youre not more popular simply because you absolutely hold the gift.

https://wikimapia.org/external_link?url=https://andypaintingservice.co.uk/service-areas/

This blog was… how do you say it? Relevant!! Finally I have found something that helped me. Thanks a lot.

https://www.noobaa.com/

You’re so awesome! I do not think I have read anything like this before. So wonderful to discover another person with a few unique thoughts on this subject matter. Really.. thank you for starting this up. This web site is something that’s needed on the web, someone with some originality.

https://accountlearning.com/

I couldn’t refrain from commenting. Perfectly written!

http://accountlearning.com/

I’m more than happy to discover this web site. I need to to thank you for ones time just for this fantastic read!! I definitely loved every little bit of it and I have you saved to fav to look at new stuff on your site.

https://childcentre.info/

I think one of your advertisements triggered my internet browser to resize, you might want to put that on your blacklist.

https://www.hulkshare.com/mortensenknowles7882/

I blog often and I seriously thank you for your content. This great article has truly peaked my interest. I will book mark your website and keep checking for new details about once per week. I opted in for your RSS feed too.

http://childcentre.info/

Good web site you have here.. It’s hard to find high quality writing like yours these days. I honestly appreciate people like you! Take care!!

https://gonm.biz/

I precisely wanted to thank you so much once again. I’m not certain what I might have used without the suggestions documented by you concerning such topic. This has been an absolute horrifying circumstance in my circumstances, however , looking at a well-written mode you processed that forced me to jump with gladness. Now i am thankful for the guidance and thus hope you are aware of a great job you happen to be undertaking instructing people by way of your web blog. I am sure you haven’t encountered any of us.

https://blogs.cornell.edu/advancedrevenuemanagement12/2012/03/28/department-store-industry/comment-page-7493/

disco lights with built-in laser x-y scanner are the coolest stuff that you can add to your disco room,

https://www.credly.com/users/hellburma0

Congress to take steps requiring the Federal Reserve to do so.

https://ozrvgm47aemxdp.gallery.ru/

Very good post! We will be linking to this particularly great content on our site. Keep up the good writing.

http://petheven.com/

You should be a part of a contest for one of the best sites on the internet. I will recommend this website!

https://www.noobaa.com/

Very nice work with your entry. Many readers may view it in the same light for sure and wholly agree with your idea.

http://list.ly/gasengineers633

i would love to enter my baby on a baby contest because she is very nice and talented;;

https://photoclub.canadiangeographic.ca/profile/21443616

Oh my goodness! Impressive article dude! Thank you so much, However I am experiencing difficulties with your RSS. I don’t know the reason why I can’t subscribe to it. Is there anybody else having the same RSS issues? Anybody who knows the solution can you kindly respond? Thanx!!

https://childcentre.info/

I want to to thank you for this good read!! I absolutely enjoyed every bit of it. I have you saved as a favorite to look at new things you post…

https://childcentre.info/

howdy, I am ranking my site higher “cb auto profits”.

https://psee.io/6svk98

ive begun to visit this cool site a couple of times now and i have to tell you that i find it quite nice actually. itll be nice to read more in the future! =p

http://doodleordie.com/profile/gasengineers888

very good post, i undoubtedly love this site, go on it

https://shorl.com/frajinunistisy

Hi there! I could have sworn I’ve been to this blog before but after looking at a few of the articles I realized it’s new to me. Nonetheless, I’m definitely delighted I found it and I’ll be book-marking it and checking back frequently.

https://gonm.biz/

Greetings! Very helpful advice within this post! It’s the little changes that produce the most significant changes. Thanks a lot for sharing!

https://www.hexenmod.com/

This site truly has all of the information and facts I wanted concerning this subject and didn’t know who to ask.

http://mhpa.ge/

Predictably, as a developed nation, Japan has a better GNI (by 182,779.46, in tens of millions of USD), which is indicative that the production degree within the country is higher than that of nationwide production.

https://tvchrist.ning.com/profile/gvYdftVU

Hello there! This article could not be written any better! Looking through this post reminds me of my previous roommate! He always kept preaching about this. I’ll forward this article to him. Fairly certain he’ll have a very good read. I appreciate you for sharing!

https://limitless-solutions.it/installazioni-permanenti/digital-signage-allestimenti-temporanei-e-permanenti/

You should be a part of a contest for one of the best blogs on the web. I most certainly will recommend this web site!

https://dalebeckman.com/

Next time I read a blog, I hope that it won’t fail me just as much as this particular one. After all, I know it was my choice to read, but I actually believed you would have something useful to talk about. All I hear is a bunch of moaning about something that you could possibly fix if you were not too busy looking for attention.

http://mhpa.ge/

Hi, I do think this is an excellent website. I stumbledupon it 😉 I may return once again since I book-marked it. Money and freedom is the best way to change, may you be rich and continue to guide other people.

https://izonemedia360.com

I could not refrain from commenting. Perfectly written!

https://www.dcsaasports.org/

Good info. Lucky me I ran across your website by accident (stumbleupon). I’ve book-marked it for later!

http://emojicheap.com/

This function alone can significantly improve the efficiency and productiveness of a sales group.

https://postheaven.net/vxqb0lhauk

To figure the credit, enter the amounts you paid for this stuff on the appropriate lines of Form 5695, Part II.

https://postheaven.net/2ah1nddkjq

You should take part in a contest for one of the greatest sites on the web. I most certainly will recommend this site!

http://www.dcsaasports.org/

There are 32.15 troy ounces in a kilogram.

https://postheaven.net/uzvrwndcuj

Your style is really unique in comparison to other people I have read stuff from. Thank you for posting when you have the opportunity, Guess I’ll just bookmark this blog.

https://www.hexenmod.com/

There’s certainly a lot to find out about this issue. I like all of the points you’ve made.

https://gonm.biz/

I really love your site.. Pleasant colors & theme. Did you make this website yourself? Please reply back as I’m wanting to create my very own website and would like to know where you got this from or just what the theme is called. Thanks!

https://social-rise.com/blog/list-of-nsfw-subreddits

A motivating discussion is worth comment. I think that you should write more about this topic, it might not be a taboo matter but typically people do not talk about such topics. To the next! Many thanks!

https://www.mot-centre.com/

Great information. Lucky me I ran across your website by chance (stumbleupon). I’ve saved it for later!

https://ecrypto1.com/

I’d like to thank you for the efforts you have put in writing this blog. I really hope to check out the same high-grade content from you later on as well. In truth, your creative writing abilities has motivated me to get my own, personal blog now 😉

https://www.hexenmod.com/

You are so cool! I do not suppose I’ve truly read something like this before. So nice to find someone with a few original thoughts on this topic. Really.. thanks for starting this up. This web site is something that’s needed on the web, someone with a bit of originality.

https://supplementfind.com/

Excellent blog post. I absolutely love this website. Continue the good work!

https://www.google.com.ph/url?sa=t&url=https://gemwinaz.weebly.com/

Nice post. I learn something totally new and challenging on blogs I stumbleupon everyday. It’s always useful to read through articles from other writers and use a little something from their websites.

https://www.fedeiran.com/default.aspx?key=GEpw~gLipEa3W8MOljQXiwe-qe-q&out=forgotpassword&sys=user&cul=en-us&returnurl=https://gemwinaz.weebly.com/

This site was… how do you say it? Relevant!! Finally I have found something that helped me. Thanks!

https://rafaelhgfca.tkzblog.com/31929263/proxy-an-overview

Hi, I do believe this is a great website. I stumbledupon it 😉 I’m going to revisit once again since I book-marked it. Money and freedom is the greatest way to change, may you be rich and continue to guide other people.

https://www.series-hot.net/

Not taking a while to do any research and reaching your local social safety office can value you hundreds of rupees.

https://telegra.ph/0107-rqlcpfluodjomtay-01-07

There is certainly a great deal to find out about this subject. I like all the points you’ve made.

https://lederglitz.com/elevate-your-tech-with-icorner-apple-products-in-bulgaria

You’re so awesome! I don’t believe I’ve truly read through anything like this before. So nice to find someone with a few unique thoughts on this subject. Really.. thank you for starting this up. This web site is one thing that is needed on the web, someone with some originality.

https://www.trinitylondon.org/?URL=https://gi8vnd.com/

I truly love your blog.. Great colors & theme. Did you develop this amazing site yourself? Please reply back as I’m wanting to create my own personal site and would like to learn where you got this from or exactly what the theme is called. Thanks!

https://eurocamgirls.com

Can I simply just say what a relief to uncover somebody that truly understands what they are talking about online. You certainly understand how to bring an issue to light and make it important. More people really need to check this out and understand this side of the story. I was surprised that you are not more popular because you most certainly possess the gift.

http://cctvinstallationsdubai.com/

An outstanding share! I have just forwarded this onto a friend who had been conducting a little homework on this. And he in fact ordered me dinner simply because I discovered it for him… lol. So let me reword this…. Thanks for the meal!! But yeah, thanx for spending the time to talk about this topic here on your blog.

https://q5id.com/

Great info. Lucky me I recently found your blog by chance (stumbleupon). I have bookmarked it for later.

https://www.lesnapoleons.com/

An interesting discussion is worth comment. I do think that you should publish more about this subject matter, it may not be a taboo matter but typically folks don’t talk about these issues. To the next! Kind regards!

https://engage.bz/

Keep in thoughts, insurance coverage companies do not generate income by giving their cash away.

https://cadillacsociety.com/users/Kmvr

Your style is really unique compared to other people I have read stuff from. Thank you for posting when you’ve got the opportunity, Guess I’ll just bookmark this web site.

http://warriorangelsfoundation.org/

You’ve made some really good points there. I checked on the net to find out more about the issue and found most individuals will go along with your views on this web site.

https://fairleevt.org/

An interesting discussion is worth comment. There’s no doubt that that you should write more on this subject matter, it might not be a taboo subject but usually people do not talk about these topics. To the next! Best wishes!

https://mhpa.ge/

I really like it whenever people get together and share opinions. Great website, keep it up.

https://www.nasze.fm/adserver/www/delivery/ck.php?ct=1&oaparams=2__bannerid=218__zoneid=10__cb=49158de16f__oadest=https://vnsi4h.com/

Hi there! I simply want to offer you a huge thumbs up for the great information you have got right here on this post. I will be coming back to your site for more soon.

http://i.txwy.tw/redirector.ashx?fb=xianxiadao&url=http://new88su.com/

You should take part in a contest for one of the best blogs on the net. I will highly recommend this blog!

https://images.google.ru/url?sa=t&url=https://bet884.net/

As a matter of fact, setting appointments can be easier done with telemarketing.

https://bandori.party/user/248410/cvpetxe/

Greetings, I do believe your site could be having web browser compatibility problems. When I take a look at your blog in Safari, it looks fine but when opening in I.E., it’s got some overlapping issues. I merely wanted to provide you with a quick heads up! Apart from that, wonderful blog.

https://structurizr.com/help/theme?url=https://gamewin79.wiki

Good site you’ve got here.. It’s hard to find excellent writing like yours these days. I truly appreciate individuals like you! Take care!!

http://rahatsat.az/

An impressive share! I’ve just forwarded this onto a colleague who was conducting a little research on this. And he in fact bought me lunch simply because I found it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanx for spending some time to talk about this topic here on your website.

https://dimple1107.com/

With automated on-line registrations, individuals’ information can get transferred right into a safe database not solely decreasing appreciable manual work but in addition providing accurate info equivalent to actual meals preferences of attendees.

https://git.iws.uni-stuttgart.de/nfulxce

The reply to this question surprised me greater than the rest we encountered throughout development.

https://kaeuchi.jp/forums/users/sgxgrpnbt/

Mood disorders are a class of serious mental illnesses that include depression and bipolar disorders.

http://www.iqjxi-with.xyz/blog/1737285710739

BBC Information’ a hundred Women record.

https://dkutjslaugc.blogspot.com/2025/01/iFp9UZDD61.html

Oh my goodness! Impressive article dude! Thanks, However I am experiencing issues with your RSS. I don’t understand the reason why I can’t join it. Is there anybody getting similar RSS problems? Anyone who knows the answer can you kindly respond? Thanks!!

https://q5id.com/

Nashville: Vanderbilt College Press.

http://www.speak-aqzlo.xyz/blog/1736268792353

The choice of parts will rely on your own wedding ceremony ceremony dress alongside together with your hair.

https://www.outdoorproject.com/users/amokgp-dmhn

An impressive share! I have just forwarded this onto a colleague who had been doing a little homework on this. And he actually bought me lunch due to the fact that I stumbled upon it for him… lol. So allow me to reword this…. Thanks for the meal!! But yeah, thanx for spending time to talk about this matter here on your web site.

https://rumble.com/v69dcrj-electric-resistance-electro-rock.html?playlist_id=VO_UuzW-w3g

Vermont. He died April 24, 1883 in Eaton County, Michigan.

http://www.qhyx-from.xyz/blog/1737036825632

I wanted to thank you for this very good read!! I certainly enjoyed every bit of it. I have you book marked to check out new things you post…

http://fairleevt.org/

There is certainly a great deal to find out about this topic. I really like all of the points you’ve made.

https://nolose.org/

This site definitely has all the info I wanted about this subject and didn’t know who to ask.

http://nolose.org/

Most of those overnight loans are booked without a contract and consist of a verbal settlement between events.

https://rant.li/oybtv/a-href-www-xuetu123-com-home-php

Now that you have bought everything separated, let’s begin with the hand instruments.

https://www.divephotoguide.com/user/oepjdqfjkinoxbhkhqr

About 18 million ladies are extra stressed out by facial hair (their very own, not their partners’) than they are about funds, according to a poll by analysis firm Kelton World.

https://www.outdoorproject.com/users/mevgd-tzadecs

If you donate a car to a charity that turns around and sells it, you can write off only the sale price, which might not necessarily be its fair market value.

https://designaddict.com/community/profile/JsTpROM

Consider me as your individual personal resource fairy godmother, right here to make your learning journey a heck of rather a lot simpler.

https://photoclub.canadiangeographic.ca/profile/21486452

Everyone loves it when individuals get together and share opinions. Great website, stick with it!

https://innova-drops.capsules.live/

Working professionally requires an expert internet connection, whether or not from an workplace or from home.

https://cadillacsociety.com/users/kUvFTv

Even in the U.S., where soccer generally takes a backseat to American football, there are celebrations.

https://designaddict.com/community/profile/LwwzIx

The catering and occasion planning firms are centered on providing customized companies to all of the purchasers.

https://postheaven.net/mugp2rxdi4

Insurance coverage – Most mortgages require the acquisition of hazard insurance to guard towards losses from fire, storms, theft, floods and other potential catastrophes.

https://www.laundrynation.com/community/profile/nbzrvzwr/

In an try to reach out to Military veterans, and create an interactive mechanism, the federal government has launched a cell app referred to as “Veterans Outreach App”.

https://www.party.biz/blogs/284681/402406/link

Guidelines for classification: 1) points; 2) aim difference; 3) number of goals scored.

https://www.divephotoguide.com/user/chjbvoltceewws

Once once more televised fixtures should not revealed on time.

https://designaddict.com/community/profile/bwEeGC

В современном мире беспроводных технологий power bank выступает необходимым гаджетом для обладателей смартфонов и других портативных устройств. Это небольшое зарядное устройство является автономный источник питания с встроенным батареей, позволяющий заряжать различные устройства где угодно. На рынке доступно множество моделей, включая инновационные решения, такие как [url=https://powerbanki.top/ ]Новый повербанк как пользоваться на powerbanki.top [/url], которые позволяют подзаряжать устройства даже в полевых условиях. Важными характеристиками при выборе являются емкость аккумулятора, количество разъемов, скорость зарядки и поддержка различных протоколов быстрой зарядки.

Отдельное внимание важно направить подбору power bank для iPhone, рассматривая особенности зарядки устройств Apple. Новейшие беспроводные пауэрбанки поддерживают технологию MagSafe, предоставляя максимально удобное использование с iPhone 12 и более новыми моделями. При выборе важно обратить внимание на сертификацию MFi (Made for iPhone), которая гарантирует безопасность использования устройства с устройствами Apple. Производительные модели с емкостью 50000 mAh в состоянии обеспечить до 10-12 полных зарядов iPhone, а также работают для зарядки MacBook и других ноутбуков благодаря поддержке USB Power Delivery.

Источник: [url=https://powerbanki.top/ ]https://powerbanki.top/ [/url]

по вопросам новый повербанк как пользоваться – обращайтесь в Телеграм sxl45

After I originally commented I seem to have clicked the -Notify me when new comments are added- checkbox and from now on every time a comment is added I get four emails with the exact same comment. Is there a means you can remove me from that service? Kudos.

https://xshopping.pro/

Very good article. I will be experiencing some of these issues as well..

https://fahrenheit-212.com/

We concentrate on Maritime Regulation.

https://designaddict.com/community/profile/gJZiuX

There are various people who are equipped to offer their valuable help in getting the currency exchange.

https://lfxbpc3dyon.blogspot.com/2025/01/uFhUvFTM.html

Way cool! Some very valid points! I appreciate you penning this write-up and the rest of the website is very good.

https://www.dcsaasports.org/

Inflation, or the general rise in prices of goods and services, can significantly impact FD interest rates.

https://golbis.com/user/xanksn/

Okay, so maybe your groom isn’t a fan of the swimsuit vest.

https://ityjfhfgj.blogspot.com/2025/01/RsgKlYZ.html

I’d like to thank you for the efforts you have put in penning this website. I am hoping to check out the same high-grade blog posts by you later on as well. In fact, your creative writing abilities has encouraged me to get my very own blog now 😉

https://www.dcsaasports.org/

I love it when folks get together and share thoughts. Great website, stick with it!

https://fahrenheit-212.com/

I truly love your blog.. Excellent colors & theme. Did you develop this site yourself? Please reply back as I’m planning to create my own site and would like to find out where you got this from or what the theme is named. Appreciate it!

https://prostadine.article-heaven.us/

We hope to recreate locations like Camp David, the Kremlin (and the tunnels beneath it), the bone-strewn catacombs beneath Paris, Hong Kong’s junk-filled harbor, the London underground and more.

https://www.party.biz/blogs/287026/404450/link

We shortly discovered that descriptions of recreation techniques are not any substitute for prototypes and actual implementation.

https://www.dcfever.com/users/profile.php?id=1223894

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

https://vin88.app/

Saved as a favorite, I like your blog.

https://sponsiobet.com/

Very good info. Lucky me I ran across your website by accident (stumbleupon). I have book-marked it for later.

https://www.wolfemetselwerken.nl

I need to to thank you for this very good read!! I certainly enjoyed every bit of it. I have you saved as a favorite to check out new things you post…

https://gumaktiv.capsuleslive.com/

Owen had a brother named Jay C. Springsteen who was a neighborhood builder in the Carson Metropolis space.

http://www.scene-llxb.xyz/blog/1736268614753

Spot on with this write-up, I honestly feel this web site needs much more attention. I’ll probably be returning to read more, thanks for the advice.

https://daltonrscje.blogstival.com/54346961/arthritis-rheumatology-professionals-professional-look-after-rheumatic-conditions-in-houston-and-sugar-land

Koning Beals. “Investors More and more Tap Social Media for Stock Suggestions.” U.S.

http://www.near-jyonnr.xyz/blog/1737725550448

A 3-choose California Courtroom of Appeal panel grappled with that query while reviewing a lady’s misdemeanor baby abuse conviction for leaving her 8-yr-old daughter residence alone so she may go to work when she couldn’t discover a child sitter.

https://golbis.com/user/pjyra/

Spot on with this write-up, I absolutely believe that this amazing site needs far more attention. I’ll probably be returning to see more, thanks for the information!

https://israelbdtah.digitollblog.com/32063651/sovereign-real-estate-advisors-browsing-the-massachusetts-commercial-real-estate-landscape

Everyone loves it whenever people come together and share thoughts. Great website, continue the good work!

http://gamlawyer.xyz/

Company is cash flow positive, profitable or approaching profitability.

http://www.story-zsuvh.xyz/blog/1737792916168

Our vacation spot wedding planner serves you with a proper strategy of wedding ceremony planning and facilitates you right from day considered one of the wedding planning.

http://www.agree-briibt.xyz/blog/1737794408467

Alderman, Jason. “Understanding Financial institution Fees.” Practical Money Expertise for life.

https://divisionmidway.org/jobs/author/qdktw/

Sunil Chhetri (born 3 August 1984) is an Indian skilled footballer who plays as a forward for Indian Tremendous League membership Bengaluru.

https://ixyx52mb4ttbg2.gallery.ru/

The reversed Seven of Wands card can also signify a lack of courage, self-belief, or stamina.

https://fab-chat.com/members/tGBYiB/profile/

There are lots of essential factors to note when attemping to bring a crew closer together.

https://www.laundrynation.com/community/profile/cbebfoa/

Hi there, There’s no doubt that your site could be having web browser compatibility issues. When I look at your site in Safari, it looks fine however when opening in Internet Explorer, it’s got some overlapping issues. I simply wanted to provide you with a quick heads up! Other than that, great website!

http://www.chefsausage.com/

The discipline is thus related to corporate finance, both re operations and funding, as below; and in large firms, the risk management function then overlaps “Corporate Finance”, with the CRO consulted on capital-investment and other strategic decisions.

https://rant.li/wut/a-href-wiki-sce-carleton-ca-mediawiki-schramm-wiki-api-php

It’s difficult to find experienced people about this topic, but you sound like you know what you’re talking about! Thanks

http://google.ge/url?q=https://hi88chat.com/

I blog often and I truly appreciate your information. Your article has truly peaked my interest. I will bookmark your site and keep checking for new information about once a week. I opted in for your RSS feed as well.

https://licemamas.com/

This is a topic that is close to my heart… Many thanks! Exactly where can I find the contact details for questions?

http://thesolderdr.com/

Great blog you have got here.. It’s hard to find good quality writing like yours these days. I seriously appreciate individuals like you! Take care!!

https://lostshambhala.com/

Without question, Montes were dominating their mid-size market segment.

https://rant.li/pmbki/a-href-www-hometalk-com-member-145370614-1072kpvguuqmzlink-a-a

Darth Tanis – Historic Darkish Lord of the Sith who lived at least 4000 years earlier than Star Wars: Episode IV – A brand new Hope, as Sith accounts from the year 3966 BBY describe kyber weaponry developed by him on the planet Malachor.

https://zenwriting.net/hvd1dxkqbn

The chess opening is Nimzo-Indian Defence: Normal Line (ECO code E40).

https://photoclub.canadiangeographic.ca/profile/21491806

Lightspeed is right for boutique hotels and resorts, specializing in offering a personalised guest experience.

http://www.win-mlyu.xyz/blog/1737794405133

I really like it when individuals get together and share ideas. Great blog, stick with it.

http://www.robo-apply.com/

Air-Raid Precautions (Approval of Expenditure by Essential Undertakers) (Amendment) (No.

http://www.ndocd-rather.xyz/blog/1737792921704

After exploring a few of the blog posts on your blog, I seriously like your way of writing a blog. I saved as a favorite it to my bookmark website list and will be checking back in the near future. Please check out my web site as well and tell me what you think.

https://www.porn-hub.vg/tag/หลุดน้อง-ndream/

Everyone loves it when individuals get together and share views. Great site, stick with it.

https://www.thestyle.world

There should be amicable consensus, so as not to hurt anybody’s feelings.

https://bandori.party/user/245976/lfdpqhd/

I blog frequently and I seriously appreciate your content. Your article has truly peaked my interest. I’m going to book mark your blog and keep checking for new details about once per week. I subscribed to your Feed as well.

http://www.quercusbuildingsolutions.uk/

You are so interesting! I don’t suppose I’ve truly read anything like this before. So wonderful to find somebody with a few original thoughts on this topic. Really.. thank you for starting this up. This web site is something that is required on the web, someone with a bit of originality.

https://www.maktaba-ahloulhadith.com/en/12-umm-hafsa-collection

Strategic Planning for Nonprofit Organizations.

https://designaddict.com/community/profile/cqJCNn

Or you might want to take your loved ones on a cross country trip in an RV and tow a second automobile behind you for sightseeing journeys.

https://zenwriting.net/ax9d1bj4p2

On-line Writing Workshop (previously Del Rey).

https://sei00rdsscofqk.gallery.ru/

Financial Strategies Internationale, Pakistan (Change Price Policy).

https://tvchrist.ning.com/profile/HTnnuUqy

23 of those CBSAs are often called self-representing PSUs, whose measured value modifications apply to only that PSU.

https://www.showmethesite.us/lazychicken/ActivityFeed/MyProfile/tabid/2622/UserId/706210/Default.aspx

The sector has registered an upsurge at 55.3 for April 2009 from a low of 44 in December 2008 and 49.5 for March 2009, according to ABN Amro Purchase Managers’ Index (PMI), an indicator of manufacturing activity in the country based on a survey of 500 companies.

https://www.laundrynation.com/community/profile/ugydqtsho/

If you are retired or have reached 59 1/2 years old, that is the only time that you are allowed to use the property.

http://www.bring-oaxm.xyz/blog/1737792907842

After Hamilton’s dying in August 1741, Chew sailed to London to study regulation at the Honourable Society of the Middle Temple, one of 4 Inns of Court.

https://postheaven.net/y9vq69zclq

Some other tools for online status administration is trackur, Google Alerts and Brandseye.

http://www.iovkm-fly.xyz/blog/1737794412749

And then the BSE’s Sensex index of India was started in 1986; As a result, the barometer of the Indian stock market became a pulse.

https://golbis.com/user/kqueny/

Durable Goods Orders (U.S.

https://pc6c250rwqx.blogspot.com/2025/01/DFUykz4kOX.html

Gone are the times when she lived primarily based on others’ wishes.

https://postheaven.net/dp16otammf

I need to to thank you for this wonderful read!! I certainly loved every bit of it. I have got you book-marked to check out new things you post…

https://kyotohanahotel.com/

The BCEC advises local officials and the Planning Board relating to environmental points and is a watchdog for environmental issues and opportunities.

https://postheaven.net/5cz5945y3u

Use coupon code “WILLIAM10” to get an incredible discount!

http://www.qzucv-wind.xyz/blog/1736268725340

I seriously love your site.. Very nice colors & theme. Did you create this web site yourself? Please reply back as I’m planning to create my own site and would like to find out where you got this from or exactly what the theme is named. Appreciate it.

http://heartlandsecurity.com/

This is a topic that is near to my heart… Cheers! Where are your contact details though?

http://www.radiomedic.ca/

Greetings! Very useful advice within this article! It’s the little changes which will make the greatest changes. Many thanks for sharing!

http://jjbailbondstx.com/

An impressive share! I have just forwarded this onto a friend who was conducting a little research on this. And he actually ordered me dinner due to the fact that I stumbled upon it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanx for spending the time to talk about this topic here on your blog.

https://www.quvae.com/scopus-indexed-journal

I want to to thank you for this fantastic read!! I certainly enjoyed every little bit of it. I have you book-marked to look at new things you post…

https://naganoleanbodytonic.colibribookstore.com/

After looking over a handful of the blog articles on your website, I seriously like your way of blogging. I saved as a favorite it to my bookmark website list and will be checking back soon. Please visit my web site as well and tell me how you feel.

http://www.safwaboutique.com/

Aw, this was a very good post. Finding the time and actual effort to produce a great article… but what can I say… I hesitate a whole lot and never seem to get anything done.

https://www.imgenerationx.com

Very good information. Lucky me I recently found your site by accident (stumbleupon). I’ve saved as a favorite for later.

https://www.brdetectors-dubai.com/product-category/gold-detectors/

It’s hard to come by experienced people in this particular topic, however, you seem like you know what you’re talking about! Thanks

https://hextrade.io

I appreciate the depth of research in this article. It’s both informative and engaging. Keep up the great work!

https://fitspresso.article-heaven.us/

Very good information. Lucky me I came across your site by accident (stumbleupon). I have saved as a favorite for later!

https://crypto30x.com

You are so cool! I don’t believe I’ve read anything like this before. So wonderful to discover somebody with some genuine thoughts on this subject. Really.. thanks for starting this up. This site is something that’s needed on the internet, someone with some originality.

https://www.imgenerationx.com

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://33win102.com

I’m amazed, I have to admit. Seldom do I encounter a blog that’s both educative and interesting, and without a doubt, you’ve hit the nail on the head. The issue is something which not enough folks are speaking intelligently about. I’m very happy that I came across this in my hunt for something relating to this.

http://www.decor-harmonia.com/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://33win103.com

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://b52club.icu/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://fabet.digital/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://go88.monster/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://789club.care/

bookmarked!!, I really like your site.

http://selfonlinestudy.com/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://game58.win/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://kubetvn88.com/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://thaodo.com/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://vlxx3.org/

Very useful content! I found your tips practical and easy to apply. Thanks for sharing such valuable knowledge!

https://alldayslimmingtea.article-heaven.us/

Good information. Lucky me I found your site by chance (stumbleupon). I have bookmarked it for later!

https://cryptogonow.com/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://7m7.com.co/

I couldn’t refrain from commenting. Perfectly written!

Sugarthatshirtissweet.com/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://99okcom.club/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://kuwin.net.co/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://mastersave88.com/

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

https://sv66.ninja/

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

https://sv368vn.la/

Next time I read a blog, Hopefully it won’t disappoint me just as much as this one. I mean, I know it was my choice to read, nonetheless I actually thought you would probably have something helpful to talk about. All I hear is a bunch of crying about something that you can fix if you were not too busy looking for attention.

https://wpsfioes.com/

Helpful content!

https://dev-westudy.accedo.gr/members/motherarmy32/activity/2033677/

Howdy! This article could not be written any better! Going through this post reminds me of my previous roommate! He continually kept talking about this. I will send this post to him. Fairly certain he’s going to have a great read. Thanks for sharing!

https://posta2z.com/refrigerator_repair_irvine

An outstanding share! I’ve just forwarded this onto a colleague who was conducting a little research on this. And he in fact ordered me dinner simply because I discovered it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanx for spending time to talk about this subject here on your blog.

https://pinup-casino.ws/

I was able to find good info from your content.

https://3030spinstudios.com/

Hi, I do believe your web site may be having internet browser compatibility problems. Whenever I look at your site in Safari, it looks fine but when opening in IE, it has some overlapping issues. I simply wanted to give you a quick heads up! Aside from that, wonderful site!

https://probetstrategy.com/e0b897e0b8b2e0b887e0b980e0b882e0b989e0b8b2-sbobet1688-e0b980e0b882e0b989e0b8b2e0b983e0b88ae0b989e0b89ae0b8a3e0b8b4e0b881e0b8b2e0b8a3-2/

I blog often and I seriously appreciate your content. The article has truly peaked my interest. I will book mark your website and keep checking for new details about once per week. I opted in for your Feed as well.

https://cleverhandeln.online/2025/01/26/searching-any-exhilarating-society-for-on-line-slots-a-good-beginners-instruction/

You need to take part in a contest for one of the most useful blogs on the net. I’m going to highly recommend this website!

http://db.frln.cr/index.html

An outstanding share! I’ve just forwarded this onto a co-worker who has been doing a little homework on this. And he in fact ordered me lunch due to the fact that I discovered it for him… lol. So let me reword this…. Thanks for the meal!! But yeah, thanx for spending time to talk about this subject here on your internet site.

https://www.slync.io/

After I initially commented I seem to have clicked on the -Notify me when new comments are added- checkbox and from now on every time a comment is added I receive four emails with the same comment. Perhaps there is an easy method you can remove me from that service? Thanks a lot.

http://mcintoshbros.com/

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

https://sv368.consulting/

Oh my goodness! Impressive article dude! Many thanks, However I am experiencing difficulties with your RSS. I don’t know the reason why I can’t subscribe to it. Is there anybody having identical RSS issues? Anyone who knows the solution will you kindly respond? Thanks.

https://www.ldmuq.com/download

Within the landmark 1964 case New York Instances Co.

http://www.nongsong.cyou/blog/1739209172458

Winston noticed that home windows of medieval glass appeared extra luminous than these of early 19th-century manufacturing, and set his mind to discovering why this was the case.

http://www.suidang.cyou/blog/1739227587863

2, Nepomniachtchi knocked some captured items onto the ground as his fingers visibly trembled whereas searching for a transfer, clearly distraught; he resigned after another transfer with less than 30 seconds on his clock.

http://www.yuancuan.sbs/blog/1739209173158

Other services, like SugarSync and Mozy, focus more on automatically backing up your vital data and storing it, fairly than making it simply accessible on-line.

http://www.enghong.cyou/blog/1739227598860

Everyone loves it whenever people come together and share views. Great site, continue the good work.

https://www.fiverr.com/seosupremacy/manually-build-100-high-pr-gov-and-edu-wiki-backlinks

I would like to express thanks to you just for rescuing me from such a circumstance. Because of exploring through the online world and meeting recommendations which were not helpful, I figured my life was done. Being alive devoid of the strategies to the issues you have solved all through the write-up is a serious case, and ones which might have adversely affected my career if I hadn’t discovered your web blog. Your primary ability and kindness in handling every aspect was very useful. I am not sure what I would’ve done if I had not come upon such a step like this. I am able to at this time look forward to my future. Thank you so much for this skilled and amazing help. I won’t hesitate to recommend your web sites to any person who desires support about this subject matter.

https://www.twidloo.com/united-kingdom/london/local-services/seo-for-plumbing

You should participate in a contest for among the best blogs on the web. I’ll advocate this web site!

https://zh.etvplayvideos.com/5XJErISPdPU/SEO-for-Plumbing

Hi there, I believe your web site might be having browser compatibility issues. When I look at your site in Safari, it looks fine but when opening in Internet Explorer, it has some overlapping issues. I simply wanted to provide you with a quick heads up! Other than that, wonderful blog!

https://sites.google.com/view/sistema-contable-empresarial/inicio

This depreciation will not be associated with an alternate of cash, subsequently the depreciation is added back into web earnings to remove the non-money exercise.

https://www.sitejabber.com/users/nuidzephoq

I was able to find good advice from your blog articles.

https://skyjournals.org/

I used to be able to find good info from your blog posts.

https://rentry.co/wbsn2f5y

Recreation 9: Topalov’s king is in hassle, but Anand, who had already missed an earlier win over 20 moves in the past, let him off the hook with 64.

https://www.gta5-mods.com/users/MbVB

Private equity funds have become a safe bet for companies looking to get money for business plans.

https://leetcode.com/u/bqormsshej/

Very good post. I absolutely appreciate this site. Keep writing!

https://cohhe.com/

With a Roth IRA, you pay taxes upfront, but your retirement investments grow tax-free.

https://unsplash.com/@vuvsmqmerioc

After looking over a few of the blog posts on your site, I seriously like your way of blogging. I book marked it to my bookmark website list and will be checking back soon. Please check out my web site as well and let me know how you feel.

https://aivideohub.blogspot.com/

Consider it or not but the insurers might hesitate to give you a comprehensive coverage in the event that they find something that makes you uninsurable, which suggests an current medical condition, life threatening hobbies like skiing and changing into unfit to work as a result of a disastrous accident.

https://wallhaven.cc/user/PVMAfsqT

Very good write-up. I definitely appreciate this website. Stick with it!

https://xnxx.beeg.us.com/?sRedir=2

There’s certainly a great deal to know about this subject. I like all the points you’ve made.

https://groundingwellcoupons.com

I would like to thank you for the efforts you’ve put in penning this blog. I am hoping to check out the same high-grade blog posts from you in the future as well. In truth, your creative writing abilities has inspired me to get my own, personal blog now 😉

https://zoptima.com/contact/

Hi, There’s no doubt that your website may be having web browser compatibility issues. Whenever I take a look at your site in Safari, it looks fine however, if opening in I.E., it’s got some overlapping issues. I merely wanted to provide you with a quick heads up! Other than that, fantastic site.

http://lilluminata.it/?URL=https://sites.google.com/view/appsodo666

Pretty! This has been a really wonderful article. Thanks for providing these details.

https://www.pharazones.com/

Your style is unique compared to other folks I’ve read stuff from. Thank you for posting when you have the opportunity, Guess I will just book mark this web site.

https://ctls.co/mail/click?id=mmail_5d5c545848f16_357584979&url=https://storiesofsanctuary.co.uk/

Nice post. I learn something totally new and challenging on sites I stumbleupon everyday. It’s always helpful to read through content from other authors and practice something from other sites.

https://participa.economiasocialcatalunya.cat/profiles/ga6789paypticket/timeline

Hi! I simply would like to give you a huge thumbs up for the great info you have right here on this post. I am returning to your site for more soon.

https://aras-sara.ca/

Excellent post! We will be linking to this great content on our website. Keep up the great writing.

https://www.imgenerationx.com

This is a topic that is close to my heart… Cheers! Exactly where can I find the contact details for questions?

https://www.etsy.com/listing/1704931521/alexandrite-earrings-color-changing

Greetings! Very useful advice within this post! It’s the little changes that make the most important changes. Thanks for sharing!

https://myrtlebeach.newsnetmedia.com/story/52406999/best-used-cars-under-20000-discover-how-to-find-reliable-affordable-vehicles-without-the-stress

A complete method is needed to address and mitigate the opposed effects of air pollution on psychological health.

http://www.would-qzet.xyz/blog/1740202478362

Spot on with this write-up, I absolutely think this web site needs a great deal more attention. I’ll probably be returning to see more, thanks for the info!

https://www.americanpsychcare.com/

Your style is so unique compared to other people I have read stuff from. Thank you for posting when you’ve got the opportunity, Guess I’ll just book mark this site.

https://geek-barvape.com/

This is the right web site for everyone who really wants to find out about this topic. You realize a whole lot its almost tough to argue with you (not that I really would want to…HaHa). You certainly put a brand new spin on a topic which has been discussed for many years. Great stuff, just great.

https://store.steampowered.com/app/3484300/DREADZONE/

Under the intense heat of the summer sun, dark shingle roofs can reach temperatures of 150 degrees Fahrenheit (65.5 degrees Celsius).

https://hackerone.com/poh7nqw5xvhr

Nice post. I learn something totally new and challenging on sites I stumbleupon everyday. It’s always exciting to read articles from other writers and practice something from their sites.

https://aircleanmaster.com/e0b8a3e0b8b9e0b989e0b888e0b8b1e0b881e0b881e0b8b1e0b89ae0b8a3e0b8b2e0b884e0b8b2e0b89ae0b8ade0b8a5e0b8a7e0b8b1e0b899e0b899e0b8b5e0b989/

You ought to take part in a contest for one of the finest blogs online. I’m going to highly recommend this blog!

https://calmcockpit.com

This blog was… how do I say it? Relevant!! Finally I have found something that helped me. Thank you!

https://panarmenian.net/eng/tofv?tourl=https://ok365.luxury/

You’re lastly crushed by the game and turn it off.

https://www.blurb.com/user/YSZtrlCmJqof?profile_preview=true

While lengthy used for transport, the river was made totally navigable via the Schuylkill Canal in 1825, followed by the construction of the Studying Railroad Most important Line in 1838 and the Schuylkill Department of the Pennsylvania Railroad in 1884.

http://www.rhc-style.xyz/blog/1740296219818

I’m amazed, I must say. Rarely do I come across a blog that’s equally educative and entertaining, and without a doubt, you’ve hit the nail on the head. The problem is an issue that not enough folks are speaking intelligently about. I am very happy I came across this during my search for something regarding this.

https://webwithbaby.com/

Buy her a subscription service to a flower-of-the-month membership, and she’ll receive a fresh bouquet delivered to her home each month for a full yr.

https://gdfjdfgh.blogspot.com/2025/02/yk43gaj0.html

I want to convey my passion for your generosity giving support to men and women that must have help with the concern. Your real dedication to passing the solution up and down had become rather invaluable and have frequently permitted folks much like me to achieve their targets. Your personal valuable guidelines means a great deal to me and far more to my peers. With thanks; from everyone of us.

https://www.metooo.es/u/679b790639a53d119a30160a

Oh my goodness! a fantastic post dude. Thanks However We’re experiencing problem with ur rss . Do not know why Not able to enroll in it. Will there be everyone getting identical rss dilemma? Anybody who knows kindly respond. Thnkx

https://stack.amcsplatform.com/user/vancanvas7

is there something like a free translation service that we can use online ? ,.

https://nativ.media:443/wiki/index.php?inchcone467

I like this web blog very much, Its a really nice place to read and get info .

https://atoms-demo.qualica.co.jp:443/atomswiki/en/index.php?mcnallychurchill257650

You’re so interesting! I do not think I’ve read a single thing like this before. So good to discover someone with a few unique thoughts on this subject. Seriously.. thanks for starting this up. This web site is something that’s needed on the web, someone with a little originality.

https://www.safwaboutique.com/de/

It’s appropriate time to make some plans for the future and it is time to be happy. I have read this post and if I could I want to suggest you some interesting things or suggestions. Maybe you can write next articles referring to this article. I desire to read more things about it!

https://wikimapia.org/external_link?url=https://holbornacinstallation.co.uk

May I just say what a relief to find somebody who genuinely understands what they’re discussing over the internet. You definitely understand how to bring a problem to light and make it important. More people need to check this out and understand this side of the story. It’s surprising you’re not more popular since you most certainly possess the gift.

https://www.safwaboutique.com/

Oh my goodness! Amazing article dude! Thanks, However I am experiencing issues with your RSS. I don’t know the reason why I can’t join it. Is there anybody getting the same RSS issues? Anyone that knows the answer can you kindly respond? Thanks.

https://www.maktaba-ahloulhadith.com/en/

Hello” i can see that you are a really great blogger,

https://hub.docker.com/u/geesepart6/

Historically, PWC two-strokes have had no pollution-management devices in any respect.

http://www.iluvbj-hope.xyz/blog/1740296641992

I always visit your blog and retrieve everything you post here but I never commented but today when I saw this post, I couldn’t stop myself from commenting here. Fantastic article mate!

https://www.fcc.gov/fcc-bin/bye?https://mileendacinstallation.co.uk

The bobcat is a North American cat which can be found from as far north as Southern Canada all the method to Central Mexico.

http://www.interview-td.xyz/blog/1740462589757

howdy, your websites are really good. I appreciate your work

https://kingranks.com/author/stentoft-goldberg-2249830/

Excellent post. I will be dealing with some of these issues as well..

https://systemcentercentral.com/

Greetings! Very useful advice in this particular post! It’s the little changes that make the most significant changes. Thanks for sharing!

https://www.assohqe.org/

This sort of considering develop change in an individual’s llife, building our Chicago Pounds reduction going on a diet model are a wide actions toward making the fact goal in mind. lose weight

https://vesttie3.bravejournal.net/troubleshooting-common-air-conditioning-issues-a-diy-overview

Very good post. I definitely love this website. Stick with it!

https://askewprov.com/

hi! cool!! if you have a second check us out, all about DreamWeaver and computers! take care!!

https://gaiaathome.eu/gaiaathome/show_user.php?userid=535692

Good day! I simply would like to offer you a huge thumbs up for the excellent information you’ve got here on this post. I’ll be coming back to your web site for more soon.

https://www.doingfootwear.com/shoe-making#how-to-make-shoes how to make shoes

Spot on with this write-up, I actually think this site needs far more attention. I’ll probably be back again to see more, thanks for the info!

https://www.dmvshoes.com/fucktrump.html#/

I have not checked in here for a while as I thought it was getting boring, but the last few posts are really good quality so I guess I will add you back to my daily bloglist. You deserve it my friend.

https://www.pinterest.com/dayelbow5/